|

However, this year it looks like things are about to change.

Short-term speculation

According to market statistics, in the last ten years, every year there has been at least one increase in December with different amplitudes. For instance, in 2014 the VN Index increased by 5.29 percent but only 1.85 percent in 2015, and in 2017 it increased to 7.28 percent. In 2020 the Index increased to 10 percent, while in 2021 it was 5.99 percent.

There were five markets that increased in the first half of December and decreased in the second half of the month, showing an increase of 3.15 percent, and then in the last two weeks decreased by 7.15 percent. Ever since the December increase appeared, it created favorable short-term speculation opportunities. The point that creates this diversity is the timing. If the market has increased strongly at the beginning of the month, it usually slows down towards the end of the month or vice versa. Only three out of ten times in December, the market increase in the whole month.

In 2022, the market is sending unusual signals. Since the beginning of the month until now, the VN Index has only had the first two increase sessions, and since that peak, the market has decreased by about 6.8 percent until December 21. If the market repeats this scenario of falling first and rising later, investors can expect an uptrend in the last week of 2022.

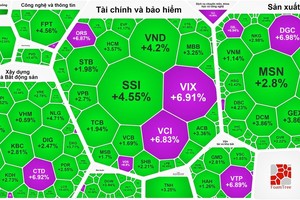

However, history does not always repeat itself. Vietnam's stock market has seen increases since November, of about 19.8 percent since the VN Index reached the lowest bottom of 873.78 points on 16 November. Hundreds of stocks have outperformed, providing an opportunity to reduce losses for many investors after a plunge of up to 32 percent since the peak in August 2022 or up to 43 percent since the beginning of the year.

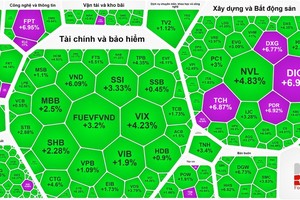

Statistics on HoSE show that there are over 300 stocks with a maximum profit margin in November and December of 20 percent or more, which is stronger than the Index. About half of these reached their maximum gain of over 50 percent. An increase of over 50 percent in less than two months should be called a tsunami, not a Tet gift. This raises the question if the market will continue to gain momentum after such an intense rally.

Some investors did not think of this as a big profit opportunity in November. Paradoxically, the stronger the bullish wave, the easier it is for investors to make a profit. When the stock price falls investors can collect losses, but on the upside, the divergence of opinion creates a chaotic crowd in the bull wave.

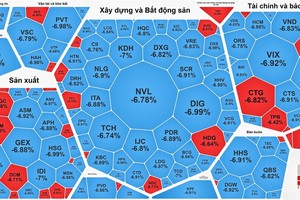

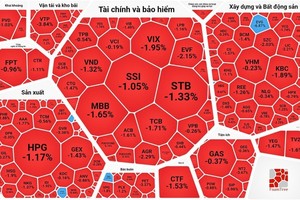

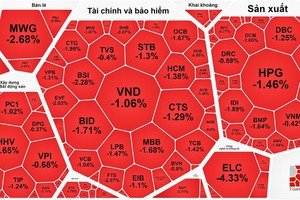

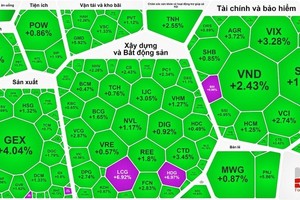

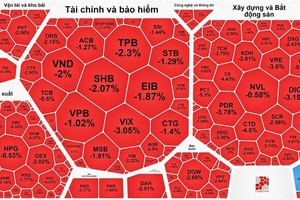

A big sell-off occurred in the first two weeks of December with the matching order size of HoSE and HNX of about VND18,000 bln per day, with the peak session on December 6 with VND24,500 bln. This is a very large transaction compared to the average size of only VND10,000 bln per day in the two weeks in mid-November when the market bottomed out. After the big profit-taking phase mentioned above, the liquidity in the last two weeks was only VND13,500 bln per day on average.

It was seen that a large amount of money was withdrawn, which is a difference compared to previous December periods. Money flow went into short-term opportunities, regardless of timing. For instance, the self-trading sector of securities companies continuously net bought since the beginning of November, and also started to net sell through order matching in the last two weeks.

Bleak forecast

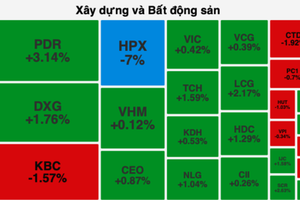

The market also expects an upward trend with quarterly business results in the fourth quarter of each year, which usually appears in January and February of the following year. However, this is also the difference in 2022, with trouble in the bonds market, a plunge in financial investments in the stock market, a high-interest rate, and a decline in exports, which all forecast a difficult fourth quarter and even a tough first quarter in 2023. Related industry groups such as real estate, banking, and exports are expected to announce fewer positive numbers. Bad debts may increase and must wait for the annual financial report to respond.

Despite the recent positive news of some banks reducing lending rates, credit room being extended, the exchange rate cooling down, real estate businesses actively buying back bonds ahead of time, and reduced capital pressure in the last month of 2022, it is still not a fundamental solution. In fact, these pressures will still persist, or even become heavier in the first quarter of 2023. The increase in domestic interest rates is temporarily limited, but the pressure to maintain high-interest rates will certainly persist as the FED maintains the process of raising the target interest rate to control rising inflation.

A highly probable risk of an economic recession hitting major Vietnamese markets such as the US and the European Union is expected to reflect on business results in the first quarter of 2023. Real estate businesses will still face difficulties. Hence the market has reason to be cautious as the stock market does not look at the present but at future risks, and when the future is uncertain for an unforeseeable time period then investors remain wary.