Illustrative photo

Illustrative photo

Bonds maturity pressure

Since the corporate bonds market began operating in 2005, the total issuance value at the beginning of the third quarter of 2022 had reached nearly VND2,500,000 bln with more than 5,000 issuances, playing an important role in providing capital for the economy. The market size has increased sharply by 140 times to about VND1,600,000 bln, equivalent to 18.3 percent of GDP and equal to 14.2 percent of the credit balance of the whole industry.

However, the corporate bonds market has only really exploded in the last three years, from 2019 to 2021. At this stage, the issuance value is up to nearly VND1,600,000 bln, accounting for 64 percent of the total issuance in the period 2005 to 2022, causing the GDP to increase from 7.3 percent in 2018 to nearly 18.9 percent in 2021. In terms of industry structure, the banking group accounts for the highest portion of corporate bonds issuance by up to 65 percent.

However, after a period of hot growth, the issuance value of corporate bonds suddenly dropped sharply in the second quarter, when Decree 153/2020/ND-CP was reviewed for amendment, with the goal of protecting the legitimate interests of investors, as well as improving quality of the capital market. According to statistics, in the last nine months of 2022, there were 411 corporate bond issuances, including 389 individual issuances, with a total issuance value of VND244,191 bln, down 67.7 percent over the same period last year. By the end of the third quarter, the outstanding debt of corporate bonds was about VND1,300,000 bln, equivalent to 13 percent of GDP in 2021.

Soon after the Tan Hoang Minh incident, many commercial banks bought back corporate bonds ahead of time. According to statistics from Vietcombank Securities Company (VCBS), the value of corporate bonds purchased by enterprises in advance was up to VND 135,180 bln after the first nine months of the year. In which, the group of Joint Stock Commercial Banks strongly bought back corporate bonds before the maturity period expired.

For instance, the Joint Stock Commercial Bank for Investment and Development of Vietnam (BID) bought back VND 12,672 bln of bonds; Vietnam International Commercial Joint Stock Bank (VIB) bought back VND8,800 bln; Lien Viet Post Joint Stock Commercial Bank (LPB) bought back VND8,000 bln; Saigon-Hanoi Commercial Joint Stock Bank (SHB) bought back VND5,450 bln; Tien Phong Commercial Joint Stock Bank (TPB) bought back VND4,900 bln; Ho Chi Minh City Housing Development Joint Stock Commercial Bank (HDB) bought back VND4,798 bln; Orient Commercial Joint Stock Bank (OCB) bought back VND ,700 bln; Vietnam Foreign Trade Joint Stock Commercial Bank (VCB) bought back VND2,900 bln; and An Binh Joint Stock Commercial Bank (ABB) bought back VND2,000 bln.

However, due to the large number of corporate bonds issued in the period from 2019 until 2021, the pressure of bonds maturity is still very intense, mainly for 2023 and 2024 with a total value of up to VND790,000 bln, and accounting for about 50 percent volume of corporate bonds in circulation. In the fourth quarter of this year, there will be about VND85,000 bln of corporate bonds nearing maturity, of which banks account for 53.4 percent.

According to VCBS, in the fourth quarter, Vietnam Technological and Commercial Joint Stock Bank (TCB) has the largest issuance value of mature corporate bonds with VND12,700 bln. Next is Vietnam Prosperity Joint Stock Commercial Bank (VPB) with VND8,000 bln; LPB with VND6,080 bln; VIB with VND3,600 bln; OCB with VND2,000 bln; Vietnam Thuong Tin Commercial Joint Stock Bank (VBB) with VND2,000 bln; HDB with VND1,800 bln; ABB with VND1,600 bln; BID with VND1,178 bln; Bac A Commercial Joint Stock Bank (BAB) with VND1,000 bln; and Vietnam Maritime Commercial Joint Stock Bank (MSB) with VND800 bln.

Investors panic

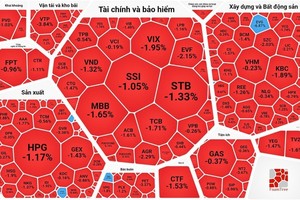

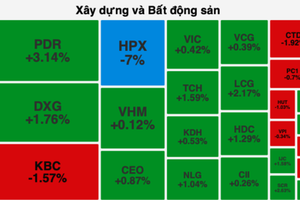

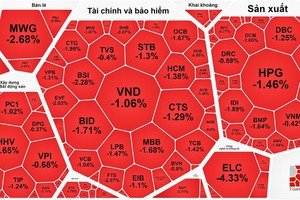

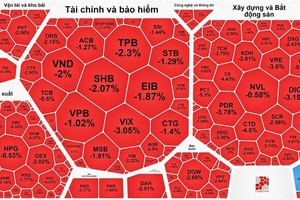

Under this great pressure, TCB bank stock was sold out strongly by shareholders and fell to the lowest price range in more than two years. Since the beginning of October until now, TCB has had 11 losing sessions, of which 5 sessions dropped to the floor. TCB stock price also plummeted, from VND32,500 to VND21,300, equivalent to a decrease of 35 percent.

Similarly, VPB had 7 losing sessions, with stock price falling from VND18,000 to VND15,400, equivalent to a 15 percent fall. LBP had 10 losing sessions, and stock prices fell from VND12,900 to VND9,350, a loss of 28 percent; VIB had 10 losing sessions and dropped from VND22,000 to VND18,850 per share, a loss of 15 percent. OCB had 8 losing sessions, dropping from VND15,300 to VND12,900 per share, and facing a loss of 16 percent; HDB had 10 losing sessions, to drop from VND19,150 to VND15,950 per share, facing a loss of 17 percent; ABB had 10 losing sessions, to fall from VND10,200 to VND7,800 and facing a loss of 24 percent; and MSB had 9 losing sessions, to suffer a drastic fall from VND16,550 to VND10,950 per share and an enormous loss of 34 percent.

The fact that this group of bank stocks was rejected by investors is an unusual phenomenon. In fact, corporate bonds issued by banks attract investors, although the average issuance interest rate is not in the highest group. This shows that the reliability and safety of the financial system are still relatively good compared to the general level of the market.

According to data issued by the Ministry of Finance, the average issuing interest rate of banks is among the lowest in the market, at an average of 4.64 percent per year. This interest rate is lower than that of the highest group of commercial and service enterprises of 10.38 percent per year, and the group of real estate enterprises are at 10.27 percent per year. Above all, with the low issuance interest rate, hard term, and issuance volume accounting for only a small portion of total outstanding loans, the issuance of corporate bonds by banks is still in a safe state, despite being under pressure of maturity in the near future.

Nonetheless, it would not be correct to say that banks do not take risks with corporate bonds, because banks are currently the main source of capital for real estate businesses. More worrisome is the fact that businesses with corporate bond balances may fall into insolvency, thereby affecting their ability to repay bank loans.

According to Rong Viet Securities Company (VDSC), with value of privately issued corporate bonds estimated at VND628,000 bln by end of 2021, equal to about 6 percent of the outstanding loan balance of the banking system, pressure on cash flow to pay the principal of corporate bonds due to maturity may still be high for the remainder of 2022.

High cash flow pressure arises in the short term, while the consumption rate of goods decreases, which leads to enterprises with high individual bond balance falling into insolvency, affecting the repayment of bank debts. In addition, individual investors holding bonds are not able to pay principal and interests on time, which indirectly causes cash flow difficulties. There is a potential risk if these individuals have loans at banks but lack stable income flow.